02-567-1349

02-567-1349 845-694-7148

845-694-7148 UPDATE: May 23, 2025

UPDATE: May 23, 2025

With current mortgage rates relatively high, everyone is looking to find mortgage products that might ease the pain of high monthly payments. Inflation Linked Mortgage (ILM) products are often thought of as a good alternative with low rates and low monthly payments. But there is more to it than that. Much more. Let’s take a look at what is really involved with inflation linked mortgages.

How Do Inflation Linked Mortgages Work?

At the end of each month, the bank takes the principal balance, multiplies that figure by the inflation rate for the month and adds that amount to the principal. It then recalculates the monthly payment based on the new, usually higher, principal balance (note: when there is negative inflation, the principal does not decrease, but remains unchanged). So, on a NIS 2 million shekel mortgage, when inflation is running at 3% (or 0.25% per month) at the end of the very first month, the bank will add NIS 5,000 to the principal balance. The mortgage payments are then continuously recalculated throughout the life of the mortgage in order to account for the impact of inflation.

When comparing ILM rates to unlinked products, this is what you may find;

– Rates on ILM’s are significantly lower than similar products that are not linked to inflation – sometimes as much as 2.0% lower. So, while a fully fixed rate mortgage might be 5%, a fixed rate ILM could be as low as 3.0%.

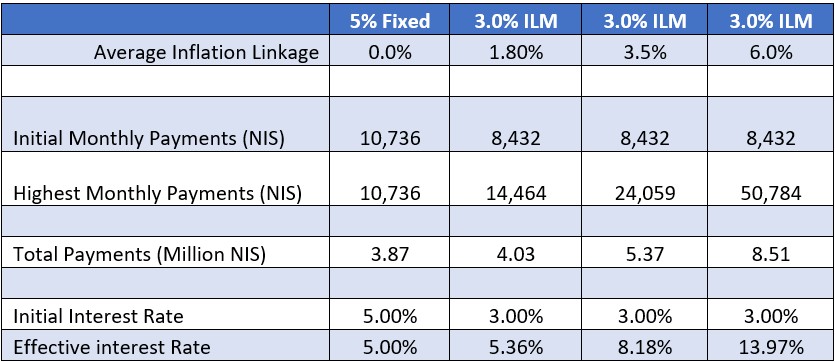

– On a 2 million shekel, 30-year, 3.0% mortgage, the ILM would result in initial monthly payments of only NIS 8,432 compared to payments of NIS 10,736 for the unlinked 5% mortgage – a significant saving.

– Before taking inflation into account, payments on the ILM would total NIS 3.04 million, compared to NIS 3.87 million for the unlinked mortgage, a savings of over NIS 800,000 over the life of the mortgage.

But let’s see what happens when the linkage starts to kick in.

The average inflation rate over the last 20 years has been approximately 1.8%, and is a good number to start with.

The monthly payments would rise to NIS 10,736 (the same as the payments on the 5% mortgage) after about 14 years and at its peak would reach over NIS 14,000.

The impact of only 1.8% average inflation would add almost NIS 1 million to the total payments, more than wiping out the hoped for savings. The effective interest rate on that original 3.0% mortgage now turns out to be almost 5.4%.

Now let’s take a look at what would be the case if inflation continued at its current ~3.5% level.

Monthly payments would reach NIS 10,736 after only 7 years and peak at over NIS 24,000.

Total payments over the life of the mortgage would increase by over NIS 2.3 million.

The resulting effective interest rate would be a whopping 8.18%.

Here is a chart that will give you a frame of reference, including the unlikely event of inflation averaging 6% over the life of the same 30 year mortgage.

Negative Amortization

Another unintended consequence of the ILM is the possibility of Negative Amortization – when the principal balance on a loan is increasing instead of decreasing. It means that the portion of the monthly payment that is allocated to paying off principal is insufficient to offset the impact of the increase in principal caused by the linkage to inflation.

Using the above example with 3% inflation, the impact of linkage at the end of the first month is an increase of NIS 5,000. However, the first payment of NIS 8,432 only includes NIS 3,420 to pay off principal. Hence, the principal at the end of the first month increases by NIS 1,580. In this same scenario, the linkage increase continues to outpace principal payments for almost 8 years.

Conclusion;

While Inflation Linked Mortgages may look inviting, there is much more to them than meets the eye. The intricate mechanics of these mortgages can lead to unexpected financial burdens. When considering mortgage options, it’s crucial to account for potential inflation effects and consult with financial advisors to make an informed decision that aligns with your long-term financial goals. Remember, a mortgage is a significant commitment, and understanding the nuances can save you from unforeseen challenges down the road.